Are executor fees deductible to the estate?

Sarah Richards

Published Apr 03, 2026

Executors are responsible for filing an income tax return for the estate to report any income from probate assets. Attorney fees and executor fees are deductible on the estate income tax return. Any net income or excess deduction is distributed proportionally to the beneficiaries on a Schedule K-1 tax form.

Are executor fees deductible?

Expenditures not essential to the proper settlement of the estate, but incurred for the individual benefit of the heirs, legatees, or devisees, may not be taken as deductions. Administration expenses include (1) executor's commissions; (2) attorney's fees; and (3) miscellaneous expenses.Can you deduct executor fees on 1041?

Specifically, are executor fees deductible on Form 1041? The short and long answer here is yes. Similar to its cousin, Form 1041, Form 1041 allows a variety of expenses and deductions that can be charged against taxable income.What can be deducted from an estate?

These deductible expenses include accounting fees to prepare your final income tax return, income tax returns for your estate or trust, and your estate tax return, if necessary. They also include attorney fees, executor fees, trustee fees, and probate costs necessary to administer your property and affairs.What expenses are deductible on estate 1041?

What expenses are deductible?

- State and local taxes paid.

- Executor and trustee fees.

- Fees paid to attorneys, accountants, and tax preparers.

- Charitable contributions.

- Prepaid mortgage interest and qualified mortgage insurance premiums.

- Qualified business income.

- Trust income distributed to beneficiaries (attach Schedule K-1)

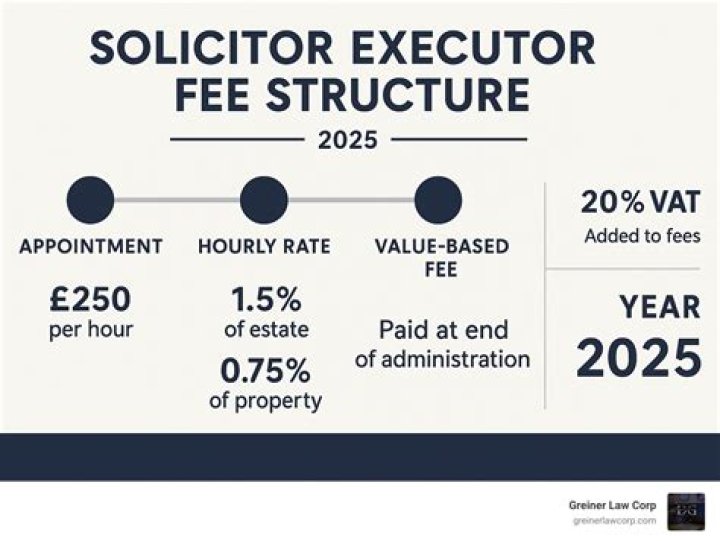

Executor Fees: Everything You Need to Know!

Are legal fees deductible on an estate 1041?

Attorney, accountant, and preparer feesAlthough Schedule A of Form 1040 limits deductibility for attorney, accountant, and return-preparer fees, Form 1041 allows you to fully deduct these fees. These fees are miscellaneous itemized deductions limited to amounts more than 2 percent of adjusted gross income.